Article

What's the Average Credit Score in America?

The Average American Credit Score, How Does Yours Compare? What is the average credit score in America? Seems like a very straightforward question, right? I agree, however while researching for this article it became very apparent that the…

4 min read

The Average American Credit Score, How Does Yours Compare?

What is the average credit score in America? Seems like a very straightforward question, right? I agree, however while researching for this article it became very apparent that the answer to that question is quite difficult to find.

A simple google search, and quick investigation of the top results left me with a slew of different answers, and frankly feeling more confused than when I began.

There are currently 3 types of scoring systems being used. Not really an issue, until you realize the scoring system used can vary depending on your lender.

FICO

Definitely the go-to where scoring is concerned, and usually the score referenced when speaking about scores in general. Your (http://www.myfico.com/crediteducation/creditscores.aspx) is based solely on information in consumer credit reports maintained at the credit reporting agencies. FICO credit scores range from 300 to 850.

PLUS Score

The PLUS Score, developed by Experian, is geared toward consumers, and not used by creditors. It runs on a 330-to-830 scale.

VantageScore

Developed a few years ago by the major credit reporting agencies (Equifax, Experian, and TransUnion) to compete with the industry-leading FICO formula. The“VantageScore”hasn't really caught with lenders and is used far less than FICO.

Instead of telling you which of the whether your Plus or Vantage score is being used, the two different types are being used interchangeable with no clear indication of where this data is coming from.

Trying to determine a national average credit score right now is pretty difficult when you take into consideration the extremely high employment rate, and the recent recession.

Those with low credit scores as a result of bankruptcy and foreclosure have seen their scores plummet further, which also drags down the national average credit score and can skew numbers quite a bit. With no immediate change on the horizon, it may be beneficial to look at things a bit differently.

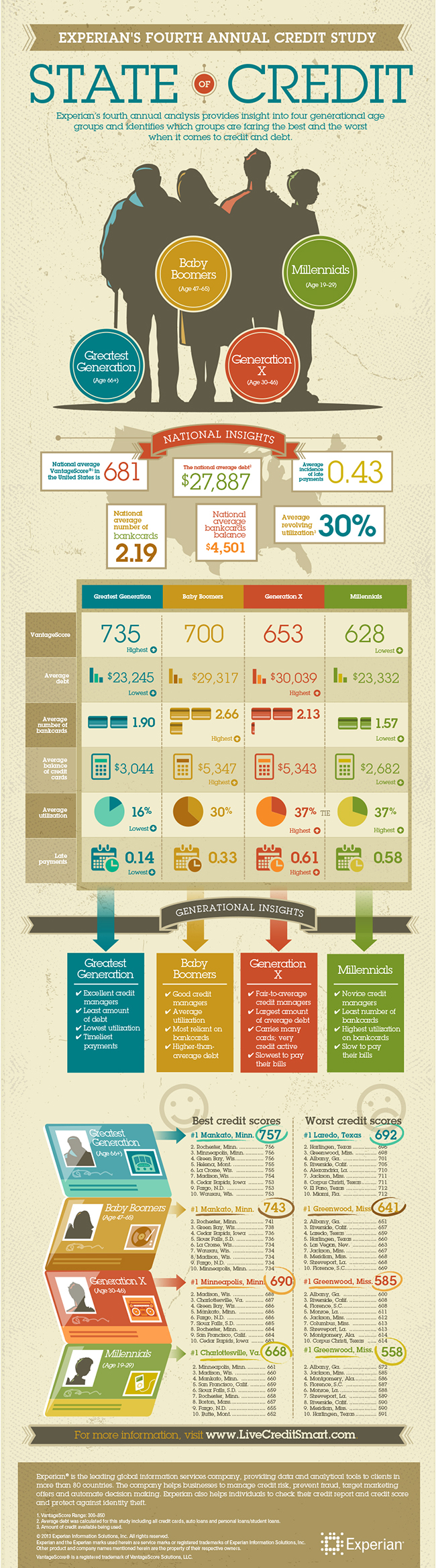

A few years ago FICO reported the average credit score in America was 723, they have been very quiet since, and haven't released an updated figure. Experian's VantageScore is a good alternative since it is updated yearly. As of the third quarter of 2014,?Experian's “State of Credit” data“reported a national average VantageScore of”681.

Experian has a great interactive, infographic illustrating their “State of Credit” findings. Highlights: The ability to see the highest and lowest scores reported in your region and the ability to see how your generation stacks up credit-wise. Overall, Mankato, Minnesota reported the highest scores for 3 of the 4 highlighted generations.

The Greatest Generation (66 +) claimed to top spot with a high of 757, and the Baby Boomers (47-65) reported a high of 743. The lowest scores belong to residents of Greenwood, Mississippi who just so happen to also be members of Generation X and the Millennials.

Generation X (30-460) reported a low of 585 and the lowest score belongs to the Milennials at 558. The following is an infographic by Experian (more information can be found at?LiveCreditSmart.com):

Following in the same line of thinking the great minds over at“CreditKarma.com”have a graph illustrating Credit Trends by Age. Their data shows what most of us already know, younger consumers usually have lower credit scores with older consumers reporting the highest scores.

The data makes sense when you take into consideration the fact that most consumers damage their credit early on with school loans. Check it out here:?(https://www.creditkarma.com/trends/age)

While there's no universal number that has been quoted as, too low a score for lenders to consent to loan you money. Consumers can expect to really feel the pinch once scores dip below 620.

According to Fico, for a 30-year fixed interest loan with a FICO score of 620, consumers can expect to pay 7.693 % interest. With a score of 619, the interest on the same loan could jump to 12.018 % [source:?(http://www.myfico.com/myfico/CreditCentral/LoanRates.aspx)\].

After the Sub Prime Mortgage fallout in 2007-2008, which resulted in a record number of loans falling into default, lenders informally raised the criteria for determining low-risk borrowers.

A score of 680 used to be enough to secure a good interest rate, as of 2008 that number jumped a whopping 40 points to 720 [source:?(http://www.zacks.com/newsroom/commentary/index.php'id)\]. So the average American according to Experian at 681, would be considered a sub-prime borrower.

Which leaves the average American with little recourse aside from remembering tips like, missing monthly payments can really damage your score, as can carrying too much debt relative to your income. The rule of 28/36 is always a good place to start.

The rule states your monthly mortgage payment shouldn't exceed 28% of you monthly gross income, and the rest of your debt shouldn't exceed 36% of that same monthly income. Applying for too much credit can also damage your credit.

Try to remember there is no right or wrong way to go about repairing or maintaining your credit. Different things work for different people. Find what works best for you, and your family.

Always key is, developing a budget and sticking to it. Once you have a handle on sticking to your budget, begin the process of assessing where your credit stands, which should bring you to a point where you are able to map out a plan for repair.

As always, use your resources and do your research. The sites referenced in this article have lots of tips and tools available as well as our website. Many consumers have found success within the forums found on these sites as well.

Forums can be a great resource, with members bouncing ideas, experiences and tried practices of each other, also providing updates and success stories along the way.